Tag Archives: debt

4 Most Common Responses to Your Debt Collection Campaigns

Running an internal debt collection campaign is essential for getting the money back that your company is rightly owed. While it is important to design your debt collection campaign to effectively reach out to clients quickly after an invoice goes unpaid, knowing what to do after your call, email or letter will help drive success.

Here are the top four most common responses businesses receive from their debt collection efforts:

Prompt payment

This is the ideal scenario. Sometimes a missed invoice is a mistake within the accounting department or the result of an employee being on vacation. If the client promptly pays after you reach out to them on a past-due invoice, always verify the following:

- The best point of contact’s name, email address and phone number

- Their preferred mode of contact for invoices (email v. mail)

Acknowledgement, with actionable response

This is the next preferred scenario after you contact a client concerning delinquency. When a client acknowledges that they are late on their payment and confirms a date they can pay their invoice, as a company you should follow-up to confirm:

- Method of payment

- If they have all of the essential information to pay (routing number, company address, etc.)

- Reason for late payment. Gathering as much information as possible for your records is important should the delinquency happen again.

Acknowledgement, but no actionable response

In this scenario, the client is aware that are late on their invoice, but does not confirm or offer a date for payment. Always reach out to the client because he or she could have forgotten to include that information in their communication with you; or they could be waiting on someone within their business to confirm a date of payment. Whatever the case may be, it is your goal to get a date set with the client. The probability of receiving payment drastically increases when you can commit the client to a specific date or payment plan.

No response

If you receive no response from a phone call, email or mailing, there may be several reasons for this.

- You may not be contacting the correct person.

- The client has a cash flow problem and has yet to find a solution. They are simply trying to avoid communication with you.

- The client is unwilling to pay the invoice and is trying to avoid you.

With any delinquent invoice, you should always follow the bad business debt timeline, which features a series of phone calls, letters and emails to engage with the client. You can find the full timeline here: http://c2cresourcesblog.com/c2c-resources-commercial-debt-collection-agency/bad-business-debt-timeline/.

What Makes a Good Debt Collector?

As a business owner, your collection call team will lead you to increasing cash flow. But is a good debt collector born with “it†or taught “it� For small businesses and start-ups, finding the right person on the team is particularly important because often team members wear multiple hats; only needing to step into the role when needed.

As a business owner, your collection call team will lead you to increasing cash flow. But is a good debt collector born with “it†or taught “it� For small businesses and start-ups, finding the right person on the team is particularly important because often team members wear multiple hats; only needing to step into the role when needed.

We think the right person has a combination of the right personality traits and proper training. Don’t always go for the sales person or accounts receivable person on the team. While they may be directly related to the process, they may not have the personality needed to deal with potentially intense situations.

When considering a team member, look for the following traits:

-Â Â Â Â Â Â Â Â Â Problem-solver: Often driven to find a solution, the problem solver is going to approach the situation with unique ideas. They will be results driven, even if the debtor becomes upset during the process.

-Â Â Â Â Â Â Â Â Â Self-motivator: Getting on a call is nerve-wracking because the debt collector does not always know how the debtor will react. By having someone with a keen sense of self-motivation, they will be driven to get the work done.

-Â Â Â Â Â Â Â Â Â Tenacity: If a debtor is persistent with providing reasons as to why they cannot pay, the collector will need to be just as persistent to make sure that the call ends with an action item of next steps in the payment process.

And, provide the following training:

-         Selling: The debt collector on your team needs to be able to prove to the debtor that they must pay. This is very similar to a salesperson’s role. By providing the team member with proven tactics you can prepare them for the most challenging calls.

-Â Â Â Â Â Â Â Â Â Customer Service: While it may be a good idea to pick the most tenacious person on the team, they also need to have good customer service skills. Being too controlling during the situation could turn the customer off and lead to no payment. The ideal candidate would have a good balance.

Finding the right person on your team to handle debt collection calls goes beyond the ability to pleasantly interact with customers. It requires a combination of skills to be effective.

Do you have the right person for the job on your team?

In Commercial Debt Collection, Should You Take a Settlement?

When collecting a commercial debt, the decision whether or not to take a settlement comes down to one thing …

In Commercial Debt Collection, sometimes a settlement is the right choice.

If it’s likely that your customer will be unable to honor an extended payment plan. To know for sure, you must find out the facts of your customer’s financial situation.

Start with a lengthy and detailed conversation with your customer. Listen intently to his explanation and take detailed notes.

While you’re on the phone, request that he send you his last 6 months worth of Merchant Statements. Once you have all the information you can get from him, take the following steps:

• Review his Merchant Statements to spot downward trends in credit card sales. Are they up or down?

• Verify the claims he’s made by contacting his other creditors. Did he tell them what he told you?

• Talk to your customer’s bank. Would a check clear if he were to issue one?

The information you gather may lead you to conclude that your customer really has no money (or too limited an amount) to pay you. If it looks to you like things are likely to continue to deteriorate, then taking a lesser amount now is better than being paid nothing later. It’s but one of the challenges of commercial debt collection.

It takes patience to do the investigative work to make the settlement decision in the process of commercial debt collection. But it’s the only way to make an informed choice.

3 Ways To A Successful Collection Call

Follow these 3 steps for a successful collection call

Debt collecting has its challenges. As the collector, you have your set of hurdles. Your past due customer has his. Both perspectives represent real people dealing with financial stresses – just trying to make the business work.

Debt collecting has its challenges. As the collector, you have your set of hurdles. Your past due customer has his. Both perspectives represent real people dealing with financial stresses – just trying to make the business work.

We rely on one another to follow through when engaging in business. Making collections calls takes a little finesse if we want to maneuver successfully through our challenges to reach a resolution. You want 2 things: To be paid and to retain the customer.

Your main objective in a collection call is of course, to be paid the same day, in full. To get there, put the following three things into action during your call.

1.   Listen intently

The more information you have about the circumstances your customer is facing, the better you’ll be able to help her resolve the debt. Give her the time she needs to explain the situation to her satisfaction. On your end, take notes and repeat the key points back to her. Consider the time this takes as an investment in your business relationship.

2.    Remain calm and professional

Regardless of how frustrating collections can be, most customers truly want to pay you. Their debt is nothing but a monkey on their back that they want gone. Typically, just listening to them talk will tell you who falls into that category. These are the kinds of customers who will respond well to helpful, useful solutions or agreements and are most amenable to your ideas.

But regardless no matter how your customer responds, staying calm and remaining professional is always the best route to take. If things heat up ~ keep your cool. Your calm responses have the potential to defuse an escalating conversation.

3.    React with firm flexibility

When you respond to your client with firm but flexible options, you open to doors to options in tough situations. This can be a relief to both you and your customer, because the fact is, while a same-day resolution is desirable, it’s not always attainable. Your customer may suggest ideas that may not be the most desirable for you. But if you’ll remain flexible and open, you may find solutions you’ve not thought of before. Once you come to a solution, be firm about the follow through.

Are your collection calls yielding results?

C2C Resources: Balanced and Fair in Debt Collections

Most of us have experienced a cash flow problem at one time or another.

Most of us have experienced a cash flow problem at one time or another.

If you’ve made more than a few collection calls, you know; it’s the number one reason for non-payment.

Even the most organized and conscientious customers can fall behind due to cash flow problems. The difficulty you face is that you have a business to run, too. How do you remain fair and balanced with good customers who are experiencing a tough time, while also being fair to your own business?

It’s possible to work with a past due customer in ways that are fair to you both. Start by allowing your customer plenty of time to tell you about the problem in as much detail as he/she will offer. Carefully listen and make notes so you can verify claims when you get off the phone. Demonstrate that you understand what’s been said by repeating the problems back to them.

If your customer offers payment solutions you’ve not thought of, remain flexible and open to ideas. If their idea for payment seems fair and reasonable for you both, put it in writing and have him sign it.

There’s always the possibility that your customer may suggest a payment plan that simply isn’t fair to you or your business. Perhaps you find it impractical or unreasonable in some way. In that case, you may find it helpful to further verify claims through other creditors who are also not being paid before you make any decisions about a payment plan. This may help you determine just how flexible you should be and if you truly want to continue doing business with this customer.

UPDATE: We add this strategy …

In your own mind, frame your collection call this way: You are a problem solver, ready to help your customer get this past due invoice off his back. It’s a financial burden! He wants freedom from it! You can help him get there by being ready with your own ideas for ways to solve the debt.

The more you demonstrate your willingness to work with your customer, the more likely you are to retain him even through this tough spot.

Take your in-house debt collection practices further with this powerful C2C Resources Debt Collection Advice.

3 Ways To Make Debt Collection Calls Easier

Calling your customer about a past due invoice can be one of the most challenging aspects of operating a business. It’s not unusual for aged accounts to pile up because business owners are uncomfortable making debt collection calls. There is a way to ease some of your own apprehension though. By doing the following 3 things, you may find the calls just a little easier to make.

1. Write down excuses

Before you pick up the phone, sit down and list out the most common reasons and excuses for non-payment you’ve heard in the past. Once it’s completed, think about your possible responses and write those down next to the excuse. Think about what worked before and what didn’t.

As an example, I’m sure you’ve heard the excuse, “The check is in the mail.†And while you hope that’s the case, you can’t know for sure, so you’ll want to press for a more concrete verification. Consider a response like, “That’s good! May I have the check number, amount and date sent so I can make sure it posts correctly?†A response like that isn’t confrontational and may result in a speedy debt recovery.

Silly as you may feel, consider rehearsing your responses out loud. This will help you think on your feet throughout the conversation.

2. Know the details of the past due account

Have the following information at hand in advance of the collections call. This will help you maintain control of the call.

How much is owed?

What are the terms of the sale?

What did they purchase?

When was the payment due?

Are there numerous open invoices?

What is their payment history with you?

3. Put yourself in a positive state of mind

A positive disposition and friendly tone of voice will help to set a good tone for an uncomfortable collection call. Take a few minutes to think positively and prepare your self for a professional, pleasant and respectful conversation. Set yourself on a slow and steady course, prepared to leave ample time for listening to your customer’s point of view without interruption.

Half the battle of making a successful debt collection call is the preparation you do before hand. Feeling like you have all your bases covered before you begin the conversation will set you more at ease and help you stay in control.

How about it? How do you prepare for collection calls?

Debt Collections Timeline: How to Stay On Track

Schedule Collection Calls and Notices using a Collections Timeline

A solid in-house collection procedure is one that carefully schedules a series of letters and phone calls that build upon one another. Having a prescribed timeline in which to send collection letters and make phone calls will help you stay organized, fair and reasonable through the course of trying to collect. Sending too few letters or not making enough phone calls may communicate that you don’t take the matter seriously.  But too many can be just as counter productive, being perceived as harassment.

You want to find that sweet spot, sending just the right amount of reminders at the right time. This can lead to successful debt recovery.

The following is a timeline we’ve built based upon a 30-day credit term. Of course, you’ll need to adjust the timeline to match your credit terms.

| Day | |

| 0 | Invoice |

| 35 | Past due reminder letter |

| 45 | Past due follow up letter on smaller accounts or initial past due call on larger accounts. If time permits on smaller accounts, a call is better than a letter at this stage. |

| 55 | Initial past due call or follow up call depending on day 45 action |

| 65 | Termination of credit letter or choose one of the 60 day demand letters |

| 80 | Final Collection call |

| 90 | Final Demand Letter |

Follow-up is a critical component to a successful collections timeline. If your client makes a promise, follow-up with a phone call if they don’t keep that promise. If you end up sending a Final Demand notice, stay true to the actions you state in it. If your letter states that you’re turning the debt over to a 3rd party collection agency, then do it.

C2C Resources helps clients with pre-formatted collection letters and call scripts through a web based recordkeeping and management software called Profit Maximizer.

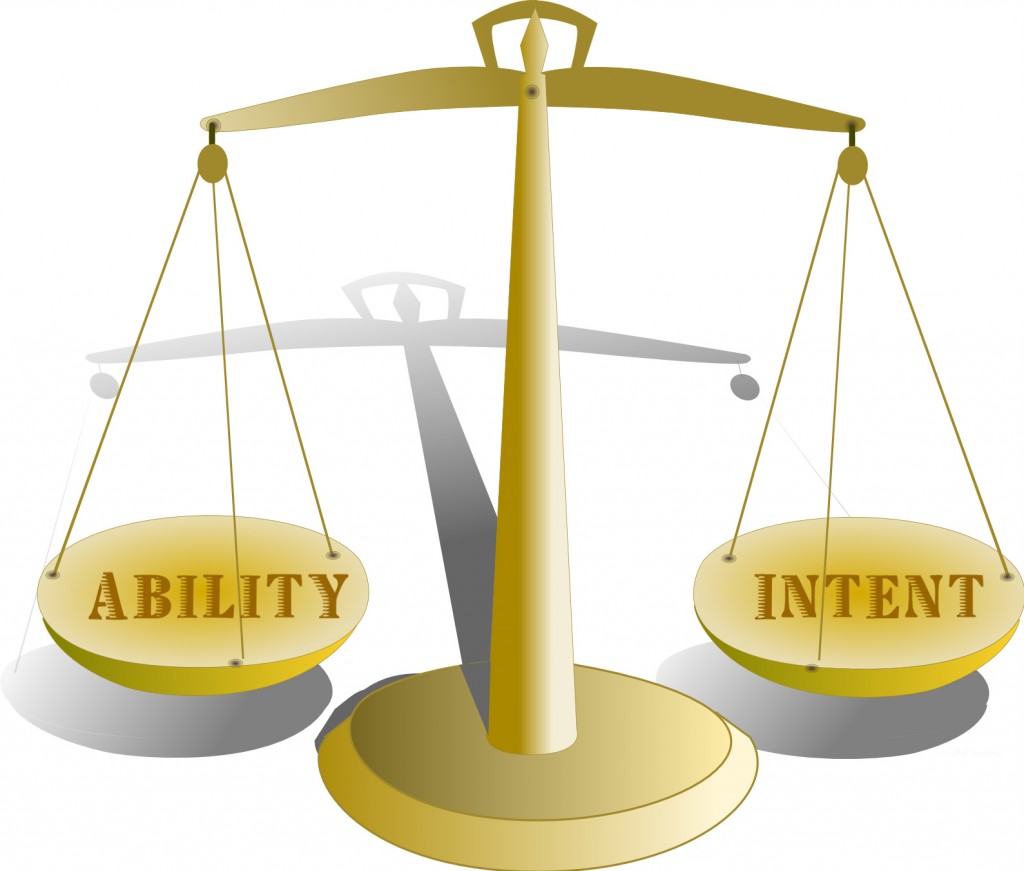

The 2 Principles to Extending Credit

There are 2 basic principles critical to the extension of credit.

1. The ability to repay a debt

1. The ability to repay a debt

2. The intent to repay a debt

If you can verify the intent of your potential customer and his or her ability to repay the debt, the decision to extend credit or not should be relatively easy. Your credit investigation should quantify ability and intent.

How do you verify the applicant’s ability to repay a debt?

Start with your applicant’s income and assets. Consider verifying their income by having them provide copies of paychecks and bank statements. When dealing in a corporate credit environment, financial statements should be enough to provide this information.

How do you verify the applicant’s intent to repay debt?

Past behavior is an excellent indicator of future behavior. A consumer credit report is a great starting point. There are many reporting agencies to choose from. Three of the larger, reputable agencies are Equifax, Experian, and TransUnion. In the corporate environment, the best way is to contact bank and trade references.

When obtaining a credit application, the applicant should provide the following information:

- Applicant Company Legal Entity Name (including any d/b/a’s)

- Corporate Address

- Telephone

- Fax

- Website

- EIN (Employer ID Number or Federal Tax Identification Number)

- Principals’ Legal Names (and SSN / DOB’s / Addresses if requiring a personal guarantee)

- Banking References including banker’s name and contact info

- Trade References (at least 3)

- CPA contact information

- Amount of credit applied for

- Requested Terms: Any special terms requiring a “meeting of the minds” (i.e. finance charges, late fees, personal guarantee, authorization to pull credit on officers, etc.)

Once the credit application is submitted, it’s imperative that you verify the information. On any point, if you find a discrepancy, discuss it with your potential customer.

- CONFIRM CORPORATE IDENTITY: For most states, the Secretary of State website provides a way for you to verify the corporate status online. Print the information and attach it to the application to keep in your customer’s file.

- PHONE NUMBER: Dial it. Did they answer with the name given or another name?

- VISIT THE WEBSITE: Print the home page and keep it in your credit file. Look for any information that may help you with your decision like press releases, news, info on suppliers/vendors, etc.

- CONFIRM EIN: There are online sites to facilitate EIN verification.

- CONFIRM PRINCIPALS: In the even that you require a personal guarantee, you may want to verify the validity of the individual’s address. If the potential risk is substantial, pull credit reports on the guarantors for further insight into their intent and ability to pay their personal debts. This could become a personal debt if the company defaults.

- OBTAIN BANKING REFERENCES: You may contact their bank and request a reference, however, the bank may decline to give you any information. If so, ask your applicant to provide a recent bank statement.

- OBTAIN TRADE REFERENCES: Naturally, people provide references they know will give a good one. However, if you look on your applicant’s website, you may find other suppliers/vendors that might give you a more objective reference.

- OBTAIN CPA INFORMATION: It’s not necessary to contact the CPA during the processing period, but should the applicant go into default, the CPA may be of value.

Make sure you document all the information you gather during the credit investigation. Keep all the information in your customer’s file. You will need it in the event that they default.

Upon completion, determine the amount of credit you are comfortable extending to your new client. Any discrepancies need to be discussed and if you feel the explanations are insufficient, you may wish to reconsider extending terms to the applicant. Any applicant hesitant about providing information should be a cause for concern.

The credit application is an invaluable tool should the customer default. Keep detailed records together with the credit app in your customer’s file. It’s and excellent idea to scan the documentation onto your hard drive, as well.